Unraveling the Intricacies of Blockchain: Benefits, Challenges, and More

In the vast universe of technological advancements, one term that has continued to gain traction in the last decade is “blockchain”. Initially associated primarily with cryptocurrencies like Bitcoin, the technology has since demonstrated its potential in a myriad of other sectors. Let’s embark on a journey to understand what blockchain is, how it works, and the pros and cons associated with it.

You can find more information about crypto here: www.cryptodash.com

1. Blockchain Technology

Blockchain technology is not just a buzzword. It represents a revolution in how data is stored, verified, and transferred. The bedrock of its appeal is the decentralized approach it brings to transactions, making them transparent, secure, and immutable. But to truly appreciate its significance, one needs to delve deeper into what a blockchain actually is.

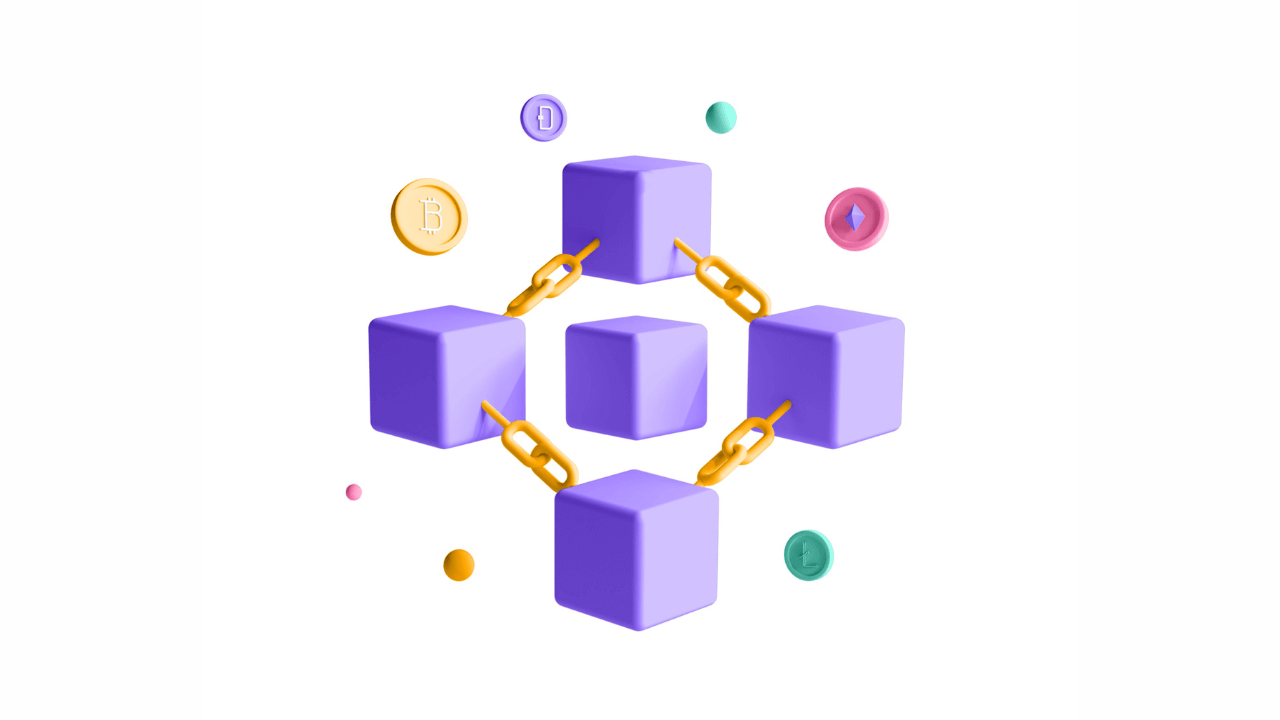

2. What is Blockchain?

A blockchain is essentially a digital ledger of transactions. Picture it as a chain of blocks, where each block contains a set of transactions. Once a block reaches its capacity, a new block is formed, linked to the previous one, thus forming a chain.

What sets it apart from traditional databases is its decentralized nature. Instead of being stored on a single server or controlled by a singular entity, copies of the blockchain are distributed across numerous computers, known as nodes. This ensures that every transaction is verified by a consensus mechanism and makes tampering almost impossible.

You can find more information about crypto here: www.cryptodash.com

3. How Does It Work?

At its core, a blockchain operates through the following steps:

- Transaction Initiation: Any user can initiate a transaction, which is then broadcast to the network.

- Verification: The network nodes validate the transaction using pre-defined algorithms. It’s worth noting that not all transactions are instantly added to the blockchain. They are initially stored in a pool and picked up by miners.

- Block Formation: Miners select transactions from the pool and form a new block by solving complex mathematical puzzles. This process is termed as “Proof of Work” in many blockchains, ensuring the validity and sequence of transactions.

- Addition to the Chain: Once the block is formed and verified, it’s added to the chain, providing a time-stamped and immutable record of the transactions.

4. Benefits and Challenges

Benefits:

- Transparency: All transactions are visible to every user, ensuring unparalleled transparency.

- Security: Transactions are encrypted and spread across a network of computers, making unauthorized alterations extremely difficult.

- Reduced Costs: By eliminating intermediaries, blockchain can significantly reduce transaction costs and fees.

- Speed and Accessibility: Transactions are processed faster than traditional banking systems, and blockchains can be accessed anytime, anywhere.

Challenges:

- Scalability: As the number of transactions increases, the size of the blockchain grows, leading to potential scalability concerns.

- Environmental Concerns: Mining, especially in proof-of-work systems, can consume massive amounts of energy.

- Regulation and Compliance: The decentralized nature can make regulatory oversight challenging, leading to potential misuse.

- Acceptance and Understanding: Despite its potential, many sectors and individuals remain wary of or uninformed about blockchain.

In conclusion, while blockchain technology offers transformative possibilities across industries, it’s essential to weigh its benefits against the challenges. As the ecosystem continues to evolve, it will be exciting to witness how blockchain reshapes our digital future.

You can find more information about crypto here: www.cryptodash.com